February 24, 2026

AI has been the most dominant technology theme for several years now. It seems to get even more attention recently as the race to AI dominance heats up and more collateral damage is left in its wake. I believe there are more folks like me who are on the fence regarding the pros versus cons of this transformative technology. Recent stock market rises and falls due to changing AI sentiment also reflect this uncertainty about the path ahead. Businesses and workers are concerned over AI-driven disruption and its impact on various industries. Investors have recently shifted their focus away from technology shares, particularly those related to artificial intelligence, as the market reacts to these sentiments. The market’s reaction to these sentiments has been a notable shift from the previous optimism surrounding AI and its potential to drive economic growth. Despite these shifts in the stock market, the global AI build-out continues to move forward.

In this part 1 article I explore how AI is not a software revolution but a physical one. Scaling AI to meet compute demand is impacting multiple ecosystems but hitting particular limits when it comes to power and electricity. I also discuss why advances in cooling, water, and data management systems are also needed to meet the growing demand for more compute and better AI systems. What resource will prove to be the most constraining over time? Learn how the AI infrastructure build-out and AI systems will change our world view, our business view, and our human view. Let me know what you think I got right and what I got wrong and where you sit on the spectrum of sentiment regarding AI. I believe we cannot defer any longer what path we choose for AI.

In this part 1 article I explore how AI is not a software revolution but a physical one. Scaling AI to meet compute demand is impacting multiple ecosystems but hitting particular limits when it comes to power and electricity. I also discuss why advances in cooling, water, and data management systems are also needed to meet the growing demand for more compute and better AI systems. What resource will prove to be the most constraining over time? Learn how the AI infrastructure build-out and AI systems will change our world view, our business view, and our human view. Let me know what you think I got right and what I got wrong and where you sit on the spectrum of sentiment regarding AI. I believe we cannot defer any longer what path we choose for AI.

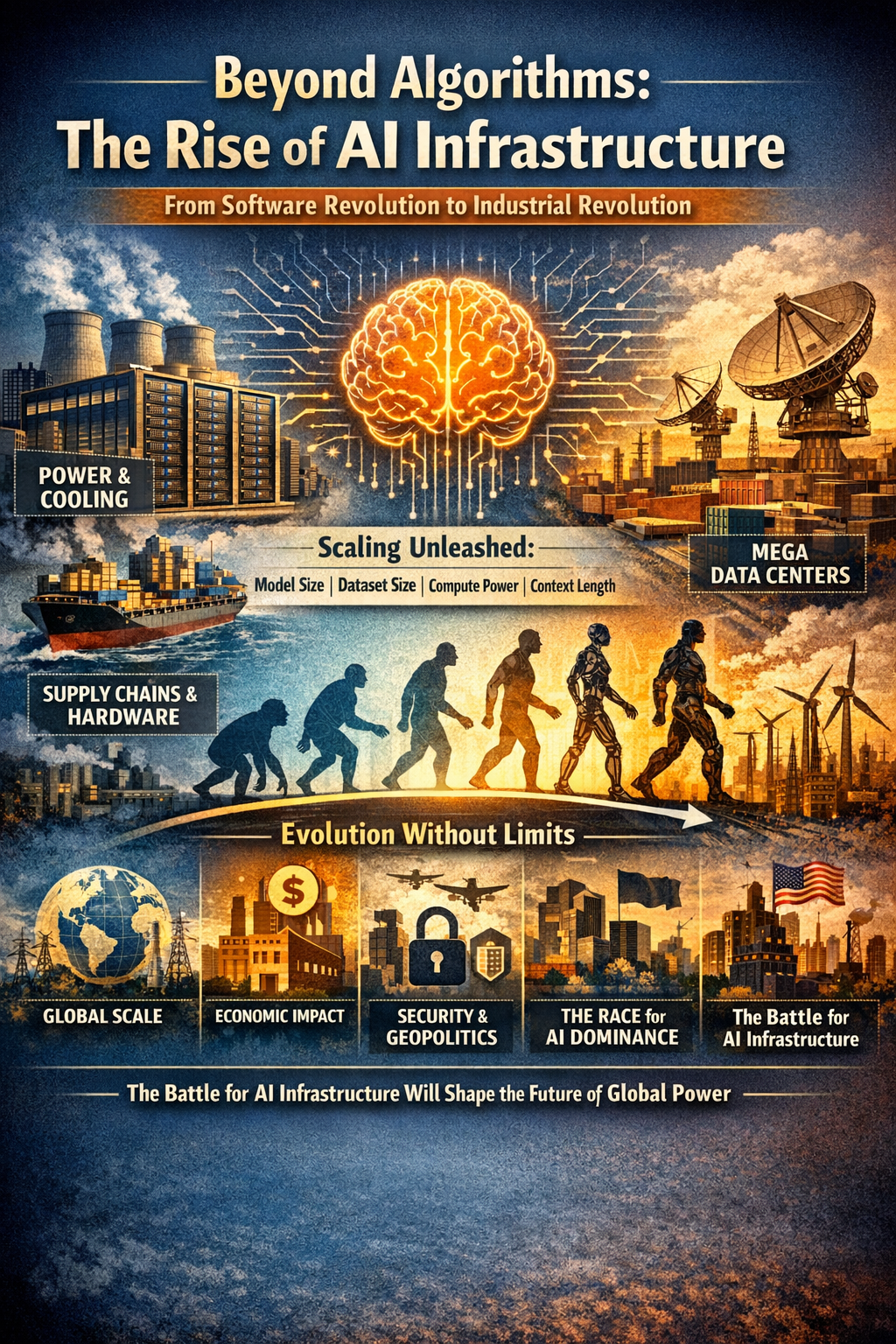

Artificial intelligence is no longer defined by algorithms alone. The real story — the one reshaping geopolitics, economics, energy systems, and the internet itself — is the rise of AI infrastructure. As models scale exponentially, the world is discovering that the limiting factor is no longer mathematical insight or data science talent. It is power, land, cooling, supply chains, and the physical machinery required to sustain intelligence at planetary scale.

The shift is profound. For the first time in history, humanity is building computational systems whose growth curves resemble biological evolution — but without the natural constraints of genetics, culture, or environment. Instead, AI scales according to new parameters: model size, dataset size, compute budget, and context length. These scaling laws, first formalized by OpenAI researchers in 2020, have become the blueprint for the entire industry.

Yet scaling comes with consequences. The world is now confronting the staggering physical, economic, and security implications of an intelligence revolution that demands infrastructure on a scale once reserved for national power grids or global telecom networks.

This article explores the forces driving the AI infrastructure boom — and the risks, bottlenecks, and geopolitical tensions emerging alongside it. It argues that AI is no longer a software revolution but an industrial one — and that the nations and organizations capable of building and securing this infrastructure will shape the next era of global power.

The New Physics of Intelligence: Scaling Laws, Data Hunger, and Physical Limits

The modern AI era rests on a deceptively simple insight: bigger models trained on more data with more compute get predictably better. Key dynamics include:

- Model size and compute scale together, producing steady performance gains.

- Sparse architectures (e.g., Mixture‑of‑Experts) reduce inference cost but do not eliminate training demands.

- Pretraining data scarcity is emerging as a critical bottleneck.

- Finetuning data quality increasingly determines downstream capability.

These power‑law relationships have held across architectures, modalities, and tasks. Models require “training” on massive datasets and their output is generated by complex neural networks probabilistically selecting words based on pattern recognition developed during the training process to create linked sentences, all without any understanding of their meaning. Generative AI systems do not “think” or “reason.” It’s just that the more data, the more precise the probability becomes of selecting the right next parameter and overall pattern.

Meanwhile, this hunger for data and compute is colliding with physical limits and threatening to stall AI growth. The world is discovering that AI is not virtual — it is intensely material. Every improvement in model capability requires:

- more power

- more cooling

- more land

- more chips

- more fiber

- more capital.

The “AI cloud” is becoming the largest industrial buildout since electrification.

The AI Data Center Race: Power, Land/Labor, and Capital Collide

Moody’s 2026 outlook forecasts a $3 trillion data center investment wave over the next five years, driven primarily by Microsoft, Amazon, Alphabet, Oracle, Meta, and CoreWeave. This investment wave is spurred by competition, but also driven by a greater goal – to be the first to reach artificial general intelligence (AGI) and super intelligence in specific fields – that is, to be the leading frontier model for government and industry. But the AI industry faces a convergence of constraints – we are running out of power, space, labor, and time with power scarcity as the defining limit.

Eric Schmidt warned Congress that AI data centers could soon require “99% of all power generated today.” While hyperbolic, the underlying trend is real: compute demand is outpacing grid capacity. McKinsey estimates that avoiding a global compute deficit by 2030 would require building twice the data center capacity constructed since 2000 — in just five years. Building enough capacity to meet projected demand would require $6.7 trillion, more than 20% of U.S. GDP.

The International Energy Agency projects that data center electricity consumption could double by 2026. IDC forecasts 857 TWh of usage by 2028. The regional locations with the greatest concentration of data centers, measured by capacity in megawatts, are (in order) Northern Virginia (an area known as Data Center Alley); Hillsboro/Eastern Oregon; Columbus, Ohio; Phoenix, Arizona; and Dallas, Texas. Data centers in Virginia currently consume 39 percent of the state’s electricity. In Oregon, it is 33 percent. The numbers, while lower elsewhere, have been rapidly climbing – in Ohio, the current share is 9 percent. In Arizona it is 11 percent. And of course, building continues; planned data-center construction or expansion is on pace to increase capacity by a third in Virginia and by more than half in Columbus, Phoenix, and Dallas.

Regardless of future activity, data-center energy use is already driving up energy prices for working people. Operators of state and regional energy grids have responded to the rise in wholesale energy prices from increasing data-center demand by passing the higher costs on to households, along with additional charges to cover new maintenance and expansion expenses.

As Bloomberg News describes:

“PJM Interconnection, the operator of the largest US electric grid, has faced significant strain from the AI boom. The rapid development of data centers relying on the system raised costs for consumers from Illinois to Washington, DC, by more than $9.3-billion for the 12 months starting in June, according to the grid’s independent market monitor. Costs will go up even more next year [2026].”

Gas and coal energy generation plants are back on. Whether net‑zero targets remain feasible given the AI arms race is an open question.

Even if the world wanted to build data centers fast enough to avoid a compute deficit, the labor doesn’t exist. Electricians — who now account for up to 70% of data center construction work — are in short supply. The US faces a severe electrician shortage, with demand far outpacing training pipelines.

And faster chips won’t save us. Quantum computing and optical accelerators hold promise, but not on the timelines required to meet today’s demand.

The result is a global scramble for energy‑dense, politically stable, skilled, and climate‑resilient regions. Norway, the U.K., and Texas are emerging as hotspots. The energy-compute nexus is pushing nuclear back into mainstream industrial planning, joining solar as the only viable long‑term solutions. The U.S. Department of Energy is even exploring leasing Oak Ridge Labs for nuclear‑powered data centers, while private companies race to deploy microreactors or small, modular reactors (SMRs) The DOE’s Genesis Mission and Data Center Nuclear Program reflect a growing consensus: AI will require a new energy paradigm. Some even propose space‑based data centers, leveraging the cold vacuum and abundant solar radiation.

Pre-certified SMRs provide a possibly faster option to get around sticky certification issues in the US, while China has much less regulatory burden in deploying nuclear power, resulting in much faster time to deployment of reactors and available power capacity. Meanwhile, there is a brain drain going on at the US Nuclear Regulatory Commission as private companies raid the government ranks to find qualified nuclear engineers. Meta is cementing its place in the “AI Arms Race” with three new nuclear deals for 6.6 GW of power.

The economics of this massive AI buildout raises concerns. The AI boom is being financed through unprecedented circular deals. Nvidia invests in OpenAI, OpenAI spends the money on Nvidia GPUs, and hyperscalers borrow billions to build data centers for OpenAI workloads. Nvidia is investing an additional $2 billion in AI cloud computing firm CoreWeave, doubling down on its long-standing (and sometimes incestuous) relationship with the company. As per the new deal, CoreWeave will be able to use Nvidia’s products before they’re available to other vendors, including a new central processing unit (CPU) and its storage systems. Whether this becomes a virtuous cycle or a bubble remains to be seen.

The pattern in Nvidia deals: Nvidia is systematically buying and investing in the control points of the data center, using its market capitalization and cash generation to pre-sell the future by seeding the ecosystem that must buy Nvidia systems.

SoftBank, Oracle, CoreWeave, and others have collectively taken on over $100 billion in debt to build AI infrastructure. Some call it an “infinite money glitch.” Others see it as the natural financing model for a once‑in‑a‑century technological shift.

The other point to be made is the lack of profit so far among these companies. Despite all the positive media coverage of artificial intelligence, as tech commentator Ed Zitron points out, “Nobody is making a profit on generative AI other than NVIDIA [which makes the needed advanced graphic processing units].” Summing up his reading of business statements and reports, Zitron finds that “[i]f they keep their promises, by the end of 2025, Meta, Amazon, Microsoft, Google, and Tesla will have spent over $560-billion in capital expenditures on AI in the last two years, all to make around $35-billion.” And that $35-billion is combined revenue, not profits; every one of those companies is losing money on their AI services.

Microsoft, for example, is predicted to spend $80-billion on capital expenditures in 2025 and earn AI revenue of only $13-billion. Amazon’s projected numbers are even worse, $105-billion in capital expenditure and AI revenue of only $5-billion. Tesla’s 2025 projected AI capital expenditures are $11-billion and its likely revenues only $100-million; analysts estimate that its AI company, xAI, is losing some $1-billion a month after revenue.

The two most popular models, Anthropic’s Claude and OpenAI’s ChatGPT, have done no better. Anthropic is expected to lose $3-billion in 2025. OpenAI expects to earn $13-billion in revenue, but as Bloomberg News reports, “While revenue is soaring, OpenAI is also confronting significant costs from the chips, data centers, and talent needed to develop cutting-edge AI systems. OpenAI does not expect to be cash-flow positive until 2029.” And there is good reason to doubt the company will ever achieve that goal. It claims to have more than 500 million weekly users, but only 15.5 million are paying subscribers. This, as Zitron notes, is “an absolutely putrid conversion rate.”

Investors, still chasing the dream of a future of humanoid robots able to out-think and out-perform humans, have continued to back these companies, but warning signs are on the horizon.

Cooling the Uncoolable: Microfluidics, Liquid Cooling, and New Materials

As GPUs grow hotter and denser due to AI compute, traditional cooling methods are hitting their limits and cooling has become a first-order engineering challenge. Air cooling hits its physical limit around 40 kW per rack. AI racks are already exceeding 100 kW. As a result, liquid cooling has become inevitable. The U.S. liquid cooling market is projected to reach $13 billion by 2032, driven almost entirely by AI workloads.

Microsoft’s breakthrough in in‑chip microfluidics — etching coolant channels directly into silicon — signals a radical shift: cooling is becoming a chip‑level design constraint. New materials and advances in power electronics also offer hope of more efficient cooling opportunities:

- Thulium iron garnet (TmIG) promises faster, lower‑power memory.

- Fuel-maker Infinium revealed a new cooling technology it described as “low-carbon dielectric liquid,”developed to deliver optimal thermal performance, stability, and safety for AI and data center environments.

- Photonic chips using light instead of electrons show 100× efficiency gains in compute energy efficiency.

- Gallium Nitride (GaN) opens the door to smaller, more efficient power convertersso that data center engineers can fit more servers in the same space, and at a lower operational cost.

While waiting for these and similar advances in cooling and heat efficient processing technology, the water use by AI data centers has surged. Data centers use potable or drinking water to protect their cooling systems from the corrosion-causing impurities and salts commonly found in non-potable sources. To make matters worse, data centers often treat the water they use with chemicals to prevent bacterial growth, making it unsuitable for human consumption or agricultural use. This means, as researchers from the University of Tulsa explain, “that not only are data centers consuming large quantities of drinking water, but they are also effectively removing it from the local water cycle.”

Large data centers already use up to 5 million gallons of water per day. That’s about the same amount used by a town of 10,000 to 50,000 people, according to the Washington-based Environmental and Energy Study Institute. Microsoft projects water consumption at its data centers will more than double by 2030, with projections of 28 billion liters in 2030, as compared to 7.9 billion in 2020 and 10.4 billion in 2024.

Data center location decisions are rarely made on the basis of water availability. The most important considerations are land prices, energy costs, and taxes. This means that many data centers are built in areas that are already water-stressed.

Cooling is no longer a facilities problem. It is a frontier of materials science, chip design, and thermodynamics with politics a big factor on the side.

The Data Problem: Scarcity, Provenance, Synthetic Data, Bias and the AI Factory

The modern AI factory is not just a training pipeline. It is a continuous feedback loop: ingest → label → train → evaluate → deploy → monitor → iterate. This requires a global data fabric with unified namespaces, parallel file systems, and intelligent data orchestration. This factory loop must include privacy-preserving technology to meet regulatory demands such as GDPR.

Problems arise, however, in the assembly and training of data, as AI systems embed their creators’ values. The reality is that AI systems are inherently influenced by human biases and values. AI is not an object but a reflection of the data, goals, algorithms, and human values that shape it. This means that while AI can be designed to be fair and unbiased, it is not possible to create and AI completely free from bias. The human factor, which is deeply embedded in the development of AI, means that biases can seep into every aspect of AI systems, from data selection to algorithm design and evaluation. It is likely that sovereign AI will also reflect a regional bias.

The data problem is further complicated. Ironically, in a world drowning in data, AI is running out of the right data – high‑quality, diverse, deduplicated, and legally usable. As the MIT Technology Review correctly puts it, “AI companies have pillaged the internet for training data.” However, often this data is rife with bias, unsure legal standing [copyright] and other problems which slow down the AI factory and create bottlenecks. To address this bottleneck some of the AI frontier model providers are taking circuitous and sometimes unethical / illegal methods to gain more data. For example, AI behemoth Anthropic downloaded a bulk of pirated fiction and nonfiction books from online shadow libraries and scanned them to train its AI models, according to documents unsealed in legal filings last week, The Washington Post reported. The company also carried out a sprawling effort, codenamed Project Panama, to buy and scan millions of physical copies of used books to accumulate troves of training data. The documents are part of a landmark copyright lawsuit that Anthropic settled out of court in 2025, shelling out $1.5 billion to pay the authors of some 500,000 books that it had illegally downloaded to train its models (Anthropic did not admit wrongdoing).

Knowing the sources of your data is becoming an important aspect of the AI factory which means capturing its provenance (not necessarily easy) or creating your own synthetic data. Synthetic data also helps to address the shortfall of “right” data. Synthetic datasets are artificially generated data designed to replicate the statistical properties and patterns of real-world data. They are created using statistical methods or advanced AI techniques like Generative Adversarial Networks (GANs), Variational Autoencoders (VAEs), and Transformer models. These datasets are widely used in machine learning, data analysis, and testing scenarios where real-world data is scarce, sensitive, or difficult to access.

Synthetic data can be categorized into fully synthetic, partially synthetic, and hybrid data. Fully synthetic data is entirely generated without real-world information, while partially synthetic data replaces sensitive portions of real data with artificial values. Hybrid data combines real and synthetic datasets to balance realism and privacy.

Synthetic data is becoming essential for:

- rare event simulation

- privacy‑sensitive industries

- anomaly detection

- performance testing

- cloud migration

- model training where real data is sparse

Synthetic data has several benefits, but it also has significant limitations:

- Bias: Synthetic data may inherit biases from the original data, which can lead to skewed results.

- Model Collapse: Over-reliance on synthetic data can degrade model performance, especially if the data does not fully capture the nuances of real-world scenarios.

- Accuracy vs. Privacy: Balancing the need for accuracy in model training with the importance of privacy is critical.

- Verification: Additional checks are needed to ensure the quality and reliability of synthetic data, as it is not real data.

These limitations highlight the need for careful consideration when using synthetic data in AI and machine learning applications. These limitations along with tighter regulatory oversight may end up causing data, not compute, to become the ultimate constraint on AI progress.

Another source of data that has the potential to be accurate and verifiable is from leveraging the underlying capabilities of the W3C self-sovereign identity. The W3C has established a Working Group to standardize the data model and syntax of Decentralized Identifiers (DIDs), which are the ID keys of self-sovereign identity. DIDs are designed to be globally unique, resolvable with high availability, and cryptographically verifiable. They are useful for any application that benefits from self-administered, cryptographically verifiable identifiers, such as personal identifiers, organizational identifiers, and identifiers for Internet of Things scenarios. DIDs are intrinsically linked to the concept of self-sovereign data, allowing users to store their data in decentralized storage solutions and grant access to applications as needed. This approach offers numerous benefits, including enhanced privacy, data portability, and reduced costs. W3C’s identity model raises a provocative question – Why shouldn’t consumers own and sell their data directly to the AI companies? Such a future data economy may require:

- Consumer-controlled data rights

- Interoperable and decentralized identity systems

- Transparent value chains (e.g., blockchains).

It could answer the data scarcity and provenance questions and help establish a way of sharing in the wealth of the AI economy.

So, what do you think about the implications of AI and where we are today in our approach to infrastructure build-out? Do you see a net positive future for the human populace as a result of AI and the race to AGI? Let me know your views on this topic. And thanks to my subscribers and visitors to my site for checking out ActiveCyber.net! Please give us your feedback because we’d love to know some topics you’d like to hear about in the area of active cyber defenses, authenticity, quantum cryptography, risk assessment and modeling, autonomous security, digital forensics, securing OT / IIoT and IoT systems, Augmented Reality, or other emerging technology topics. Also, email chrisdaly@activecyber.net if you’re interested in interviewing or advertising with us at Active Cyber™.